Resale means any sale after the first transfer of ownership (whether for consideration or not).

The scheme therefore applies to all sales after the first transfer of ownership.

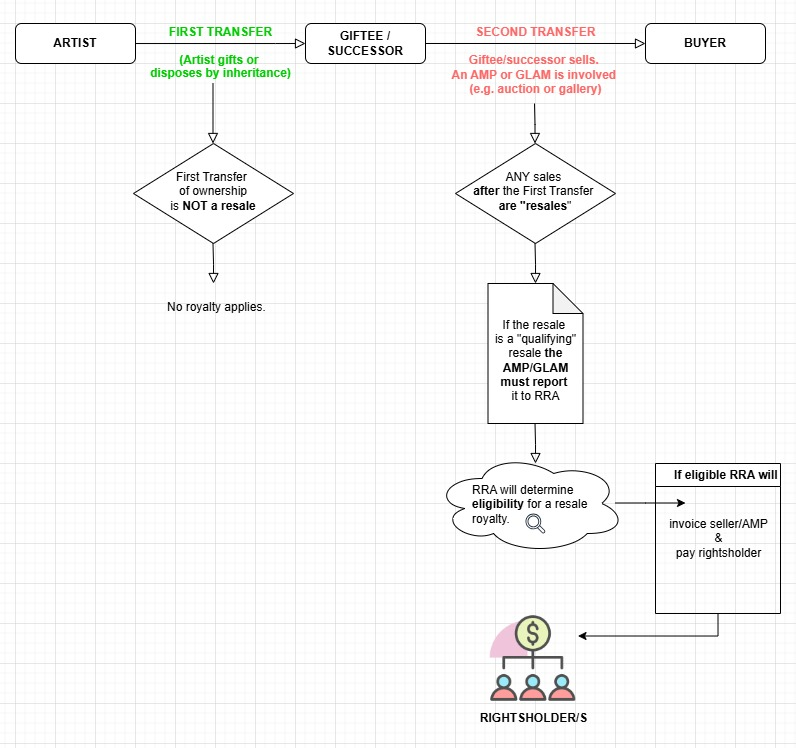

How does this apply to sales of gifted or inherited artworks?

Explained in the context of a sale of gifted and/or inherited artwork, that means:

- When the artwork is gifted by the artist, or inherited from the artist:

- This qualifies as the “first transfer of ownership”. This means the first transfer does not count as a “resale”.

- However, when the giftee or successor subsequently sells the artwork:

- This is a sale after the first transfer of ownership. This means it is a “resale”.

- This means the scheme applies to the resale. If an AMP or GLAM is involved in this resale, and the resale is over $2,000, then it must be reported to RRA as a “qualifying resale”.

For a visual representation please see the flowchart below: